Bill 142: The Law Allowing Tax Crime, Fraud And Money Laundering To Be Settled Out Of Court

- Bill 142 introduces a formal mechanism for out-of-court settlements for breaches of Malta’s tax laws and crimes committed alongside it.

- Under this framework, taxpayers may enter into agreements with the Commissioner for Tax and Customs to regularise tax offences by paying penalties and outstanding dues, thereby avoiding criminal prosecution for the offences covered by the settlement.

- The mechanism also applies to certain “connected breaches” linked to the tax offence, such as money laundering and fraud.

- Other crimes, such as bribery and abuse of authority, are excluded from the settlement framework.

- The mechanism is already being implemented. The Tax Commissioner is processing applications for administrative sanctions and fines.

- Malta has over €8 billion in uncollected taxes.

- Malta’s ability to tackle tax evasion was a reason it was placed and later removed from the FATF Grey List.

- Lawyer Aron Mifsud Bonnici, charged with money laundering, tax evasion, and making false declarations, has said he will use the mechanism.

- Laws will impact the €62 million VAT carousel fraud case and a major tax evasion case involving Nigel Scerri.

- Bill 142 passed parliament in just 12 days during July-August 2025.

- Industries in tax planning, corporate structuring, and financial transactions are classified as “medium-high” risk for financial crime and money laundering.

On 11th August 2025, Malta quietly adopted Bill 142, a piece of legislation that fundamentally rewires how the Maltese State treats tax crime and everything that flows from it.

The law does not decriminalise tax evasion on paper. Instead, it introduces a “special mechanism for out-of-court settlements” that allows tax evaders to resolve fiscal breaches without criminal prosecution.

Crucially, the mechanism does not stop at tax offences. It extends to so-called “connected breaches” – meaning crimes committed alongside tax evasion, including money laundering, fraud and conspiracy.

In practice, this means that individuals accused of multiple financial crimes can resolve all of them through administrative settlement, avoiding criminal prosecution entirely.

“This bill is going to ruin the country,” a tax consultant told Amphora Media.

The mechanism is already being implemented. In reply to a series of parliamentary questions by MP Adrian Delia, Finance Minister Clyde Caruana confirmed that the Malta Tax and Customs Administration (MTCA) has received several applications under the new law and is currently processing them.

Caruana did not say whether any fines or sanctions have yet been imposed. He also declined to provide figures on the number of individuals or companies involved, the size of those companies, or the types of businesses concerned, referring the questions to the relevant minister.

Malta already has a significant problem with uncollected taxes. Official figures show that as of 2024, Malta has accumulated over €8 billion in uncollected tax, €6.1 billion in VAT and €2 billion in other taxes. The government has written off over €6.6 billion of that figure.

Meanwhile, the FATF had expressly noted how Malta’s ability to fight tax evasion was one of the reasons the country was placed on the grey list to begin with – and was one of the three requirements to get off it.

Amphora Media has sent questions to MTCA Commissioner Joseph Caruana for further clarification on the figures.

Under the Bill 142 mechanism, available under certain conditions, taxpayers or companies who reach a settlement with the tax authorities may have their criminal liability for certain tax breaches extinguished after paying outstanding dues and an additional penalty ranging from €10,000 to €1,000,000.

In return, settlement agreements will constitute an “executive title” allowing direct enforcement, while resolving and terminating related court proceedings.

Under the settlement mechanism, once the taxpayer pays the agreed amounts, all criminal liability for the covered breaches and related connected breaches is extinguished, and any ongoing prosecutions are effectively terminated.

The changes apply to all forms of tax: Income Tax, VAT, Social Security, and Duties.

The Act also explicitly allows the Commissioner to recognise agreements entered into before the law came into force.

Connected Breaches: The Law Extends Beyond Tax Crime To Other Serious Offences

Crucially, the mechanism covers all breaches of tax laws and all “connected breaches”, that is, any criminal offences committed while breaching tax laws.

The Act defines “connected breaches” and covers offences committed to facilitate, conceal, or profit from tax crimes, including acts forming part of a pre-concerted plan or involving the use of criminal proceeds.

For example, a person who commits money laundering and fraud in pursuit of a tax crime can avoid criminal prosecution for all three charges. It would even extend to conspiracy and other serious crimes.

This is despite a national strategy (2021-2023) promising that “The legislative AML/CFT/CPF framework will be constantly updated to ensure adherence with international (FATF and European) standards, as well as other best practices worldwide”.

The law contains a narrow exclusion, providing that “connected breaches” do not include offences listed under Subtitle IV of Title III of the Criminal Code.

These include offences relating to abuse of public authority, unlawful exaction, extortion and bribery, abuses committed by advocates and legal procurators, malversation by public officers and servants, prison-related abuses, refusal of a lawfully due service, and breaches of duties associated with public office.

Offences typically associated with tax evasion, fraud, and financial misconduct remain eligible for settlement.

Under the new mechanism, limitation periods for both tax offences and connected crimes are suspended while settlement negotiations are ongoing. During this period, no prosecution may be initiated.

Under articles 187A and 187B, the amendments do criminalise breaches of government settlement agreements, with potential imprisonment and further fines (limited to €2.5 million and €500,000, respectively).

However, more consequentially, article 187C stipulates that these offences can only be prosecuted following a complaint by the Commissioner.

Bill 142: A major tax reform rushed through parliament in 12 days

In its official “Objects and Reasons”, the government framed Bill 142 as a measure designed to strengthen investigative powers, improve tax recovery, and deter financial crime.

It claimed the new settlement mechanism would impose penalties comparable to those applicable in criminal proceedings, while enhancing the state’s ability to collect outstanding dues.

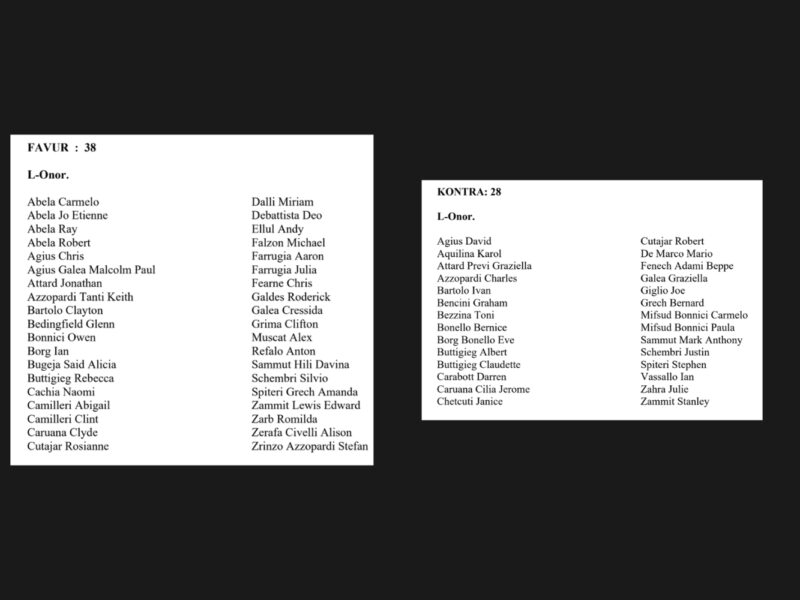

The law moved through Parliament in 12 days. Its first reading was held on 23 July 2025, and on 4th August, it passed its second reading, committee stage, third reading and final vote in a single day. All 38 government MPs supported the bill, while 28 members voted against it.

Bill 142 was tabled in Parliament on the same day as Bills 143 and 144, two parts of a controversial planning reform package that has since dominated public discourse and sparked protests. While those bills remain at the first reading stage, Bill 142 was approved and assented into law by 11th August.

Bill 142 implications: The lawyer, the VAT carousel, and the tax advisors

The law is already leaving its mark.

In September 2025, lawyer Aron Mifsud Bonnici informed the courts that he would be exploring the legal amendments enacted under Bill 142 in his case, in which he stands accused of money laundering, tax evasion, and making false declarations in documents prepared for the Malta Tax and Customs Administration (MTCA).

More than €1.6 million of Mifsud Bonnici’s assets were frozen in a court order as part of the case on 23rd July 2025.

According to a Times of Malta investigation, the probe into Mifsud Bonnici began following a series of large transfers worth €1.4 million to XNT Limited, a Malta-based investment firm.

Financial documents reviewed by Times of Malta indicated that Mifsud Bonnici received over €2.4 million in payments into his personal bank accounts between 2016 and 2019. However, during those same four years, Mifsud Bonnici declared a total income of €680,000.

Mifsud Bonnici is an associate of former minister Konrad Mizzi and is separately facing criminal charges related to the Vitals Hospital case.

He served as a legal advisor in former Prime Minister Joseph Muscat’s government; as an advisor in the Ministry for Energy under Konrad Mizzi, where he participated in discussions on the Montenegro Wind Farm Project; as the board secretary at Enemalta; and as a member of the Grievances Board at Transport Malta.

A separate Times of Malta investigation also revealed how Aron Mifsud Bonnici and Robert Borg raked in over half a million euros in “dividends” and “directors’ fees” from two companies involved in the publicly funded community work scheme.

The law could also have significant implications for a major tax fraud investigation involving a VAT carousel.

In 2023, it was reported that Martin Farrugia and Henriette Cassar were accused of defrauding the VAT system, allegedly to the tune of around €62 million.

The investigation, known as Operation Panthera, reportedly covers the period 2012–2019 and encompasses companies linked to the contractor (including NCCF, MAM Construction Ltd, and MWF Construction Ltd), which are said to have under-declared substantial sales and VAT payable.

The pair have pleaded not guilty, and the case is ongoing. Amphora Media has been informed that the police are aware of businesses involved in the scheme, but all have so far evaded prosecution.

In December 2025, Farrugia was approved a variation to his freezing order to transfer four leopards and four pumas to the Pafos Zoo in Cyprus.

Amphora Media has reached out to the police over the issue, but they have not responded.

Another case impacted by the legislation involves Nigel Scerri and his wife, Mikaela, the owners of a tax advisory and accountancy firm. The pair have been charged with money laundering, tax evasion, fraud, and other crimes, and are subject to a €15 million asset freeze.

Malta’s High-Risk Industries

A 2023 National Risk Assessment (NRA) on money laundering, referenced in the Parliament in February 2026, revealed that several key sectors remain vulnerable to financial crime despite enhanced regulatory controls.

It evaluated industries in the Financial Sector, Designated Non-Financial Businesses and Professions (DNFBPs), and Virtual Financial Asset Service Providers (VFASPs) based on three factors:

- Inherent risk: how vulnerable the sector is by nature,

- Effectiveness of mitigating measures: how strong the controls and supervision are,

- Residual risk level: the remaining risk after controls are applied.

Most sectors fell within the medium-to-medium-high residual risk range. Strong controls (rated “High” or “Substantial”) reduce risk in many areas. However, in several industries, the risk level means they still require close monitoring, and some sectors remain vulnerable to money laundering and financial abuse.

Financial Institutions, Recognition Notice Framework, Corporate Service Providers (CSPs), Real Estate (Immovable Property), High-Value Goods Dealers, and Tax Advisors also fell under the medium-high risk residual risk category.

The Finance Ministry, MTCA, the Attorney General’s Office, Aron Mifsud Bonnici, Martin Farrugia, and Henriette Cassar did not respond for request for comment.

More to read

-

Malta Under Focus In New York Times Investigation On Major US Companies And Billion-Dollar Tax Avoidance

-

-

Politics

Open Malta: A New Political Data Transparency Platform By Amphora Media

-

The Dotcom ‘Queen’ Who Fled Malta Is The Focus Of New Guardian Investigation

-

-

Environmental

Fireworks Factory Explosion: The Owners, Planning Applications, and Government ‘Safety’ Support

-

-

Politics

Which of Malta’s Election Polls Was Most Accurate?